Importer of Record Liability: Who Is Legally Responsible for Import Duties and Compliance?

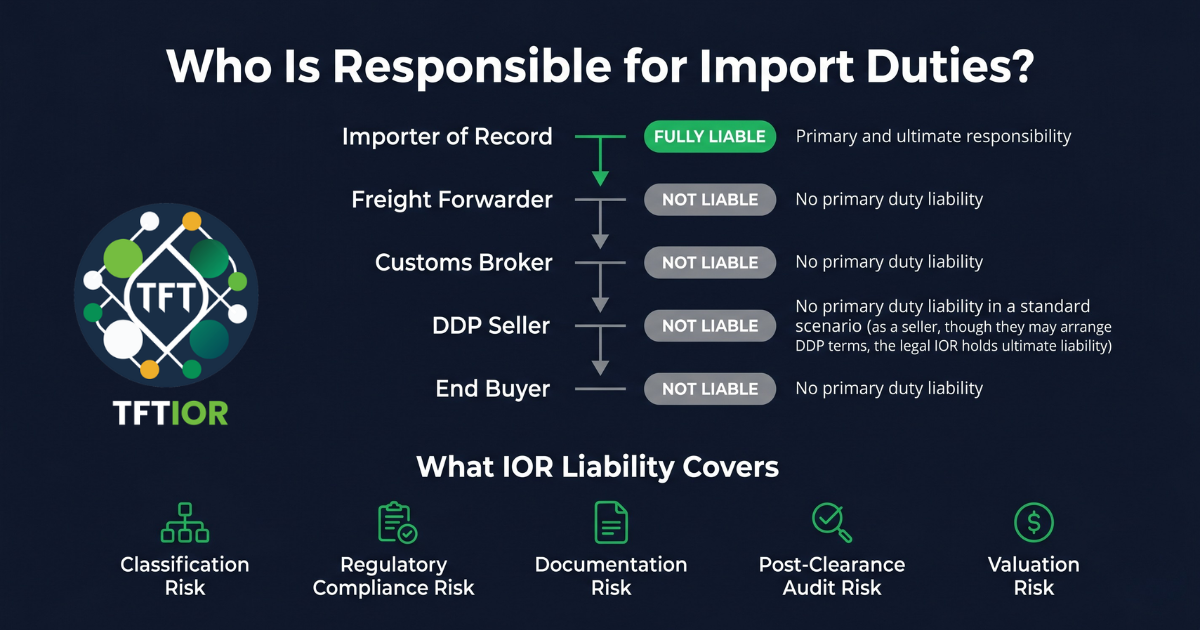

- The Importer of Record is the entity legally responsible to the destination country's customs authority for duties, taxes, classification accuracy, and regulatory compliance.

- Freight forwarders and customs brokers do not assume this liability. They are agents. The IOR is the principal.

- DDP Incoterms shift commercial cost responsibility between buyer and seller. They do not change which entity is liable under customs law.

- Incorrect HS classification can trigger retroactive duty assessments and penalties months or years after a shipment clears. The IOR bears this exposure.

- In Turkey, the penalty for a customs duty shortfall caused by misclassification is typically three times the duty difference, under Customs Law No. 4458.

- Using a paper IOR structure does not eliminate this risk. It concentrates it in an entity that may not be able to absorb it.

When a shipment enters a country, customs authorities are not interested in the commercial arrangement between the buyer and seller, who paid for freight, or what the logistics contract says. They are interested in one thing: who is the Importer of Record.

That entity carries the legal liability for the shipment. Everything else in the import chain is, from a customs law perspective, secondary.

Misunderstanding this is one of the most common sources of unexpected penalties, compliance failures, and post-clearance audit exposure in international trade. This guide explains what Importer of Record liability actually covers, where the risk concentrates, and why the distinction between legal liability and commercial responsibility matters in practice.

Who Is Responsible for Import Duties?

The Importer of Record is legally responsible for import duties under customs law, regardless of commercial payment arrangements, regardless of who arranged the logistics, and regardless of what the sales contract says. This is not a default that can be contractually overridden between private parties. It is how customs law works in virtually every jurisdiction.

What Importer of Record Liability Actually Means

Importer of Record liability is not a contractual concept. It is a customs law concept. The entity declared as Importer of Record on the customs entry takes on a set of legal obligations that exist independently of any commercial agreement between the parties involved in the transaction.

These obligations include the accuracy of the customs declaration, the correct classification of goods under the Harmonized System, payment of applicable duties and taxes, compliance with destination-country import regulations, and full accountability in any post-clearance review, audit, or enforcement action initiated by customs authorities.

Customs authorities in most jurisdictions deal with a single responsible party per import entry. If the declaration contains errors, if regulatory requirements were not met, or if duties were underpaid, that party is the Importer of Record. The authority does not trace back through logistics chains, commercial contracts, or Incoterms to allocate responsibility across multiple entities.

Liability vs Payment: A Critical Distinction

In international trade, the party that pays import duties is not necessarily the party legally responsible for them. This distinction matters more than most procurement teams realize.

- Payment can be contractually assigned between buyer, seller, or a third party.

- Liability cannot be outsourced. It follows the entity named as Importer of Record on the customs entry.

Customs authorities pursue the Importer of Record, regardless of who funded the duty payment. If an audit finds underpayment or misclassification, the assessment goes to the IOR, not to the party who wrote the check.

Who Does Not Carry the Liability

The most persistent source of confusion in import structuring is the assumption that operational involvement in a shipment translates to legal responsibility for it. It does not.

A customs broker files the declaration, but they do so on behalf of the Importer of Record and as their agent. If the information in that declaration is incorrect, the liability does not sit with the broker who submitted it. It sits with the entity in whose name the import was made.

The same logic applies to freight forwarders. Coordinating transport, managing warehousing, handling documentation handoffs: none of these functions constitute import liability. Forwarders are logistics operators. They are not legal importers.

This distinction is frequently misunderstood in import structuring decisions. For a detailed comparison of how these roles differ in practice, see our guide on Importer of Record vs Customs Broker.

Why DDP Terms Do Not Remove Import Liability

DDP, or Delivered Duty Paid, is one of the Incoterms published by the International Chamber of Commerce. Under DDP, the seller agrees to bear the cost and responsibility for delivering goods to the named destination, including customs clearance and duty payment.

This is a commercial agreement between the buyer and seller. It does not alter who is named as Importer of Record on the customs entry, and it does not transfer legal liability under customs law to the seller unless the seller is also the declared Importer of Record in the destination country.

In practice, a seller shipping DDP into a country where they have no legal presence often cannot be named as IOR, because most jurisdictions require the Importer of Record to be a locally registered entity. This creates a common structural problem: the seller agrees to DDP terms, the buyer assumes this includes customs handling, and neither party has properly established a compliant IOR structure. The shipment may clear, but the compliance liability sits with an entity that may not be equipped to handle it.

Incoterms define cost allocation. Customs law defines liability. These are separate frameworks, and conflating them is a consistent source of compliance exposure in cross-border trade.

What the Liability Actually Covers

IOR liability extends across several risk categories that can create exposure before, during, and well after a shipment clears customs.

Every import declaration requires the goods to be classified under the Harmonized System. The applicable duty rate, the regulatory regime, and any required approvals all flow from that classification. Incorrect classification, whether intentional or a genuine error, triggers retroactive duty reassessment and potentially significant penalties. In Turkey, under Customs Law No. 4458, the administrative penalty for a duty shortfall caused by misclassification is typically three times the difference between what was paid and what was owed. Post-clearance audits can surface classification errors years after clearance. The Importer of Record is responsible in all cases.

Many product categories require specific approvals, certifications, or licenses before they can legally enter a country. Telecom and networking equipment typically requires type approval from a national authority: BTK in Turkey, MCMC in Malaysia, RATEL in Serbia, NTRA in Egypt. Medical devices require pre-market registration or health ministry clearance in most markets. Refurbished IT equipment requires licensed import pathways in markets including Turkey, Brazil, and Vietnam. The Importer of Record is responsible for ensuring these requirements are met before the shipment moves. A shipment that clears through an incomplete approval pathway remains non-compliant, and the IOR carries that exposure.

Customs declarations must be supported by accurate commercial documentation: invoices that reflect actual transaction value, packing lists that match the physical shipment, and certificates of origin where required. The IOR is accountable for the accuracy of the documentation package, not solely the party that produced it.

Customs authorities actively monitor undervaluation patterns. If declared values fall below expected benchmarks, shipments may be flagged for inspection and reassessed. Multinational companies face particular exposure when transfer pricing adjustments or royalty payments are not correctly reflected in the customs value declaration. The Importer of Record is responsible for ensuring declared value reflects actual transaction value under the destination country's customs valuation rules. Post-clearance audits regularly surface valuation discrepancies months or years after clearance, and the resulting assessments can exceed the original duty payment significantly.

Customs authorities in most jurisdictions have the power to audit import declarations after goods have cleared and entered circulation. The audit window commonly extends to three to five years from the import date, and in some cases longer. Audits can be triggered by risk profiling, sector-wide enforcement actions, or third-party information. When customs authorities review past imports and identify errors in classification or valuation, the Importer of Record faces retroactive duty assessments, penalty calculations, and in cases of systematic non-compliance, potential criminal referral. Clearance at the time of import does not establish finality of the compliance position.

Customs authorities in several markets, including Turkey, have intensified retrospective review of importers whose history shows patterns of valuation discrepancies or classification inconsistency. Companies identified through these reviews may be placed on enhanced scrutiny lists, face suspension of expedited clearance privileges, or encounter systematic inspection of all subsequent entries. This risk extends to both the Importer of Record and, in some enforcement frameworks, the exporter named on the original shipments. Operational disruption from systematic inspection can materially affect project timelines for companies dependent on regular cross-border equipment deployments.

How This Plays Out in Practice

The mechanics of IOR liability are easiest to understand through the sequence of events that follows when something goes wrong.

- A shipment of networking equipment enters a regulated market. The HS code used during clearance reflects a lower duty rate than the correct classification would attract. The declaration is accepted and the goods clear.

- Months later, the customs authority initiates a post-clearance audit of the importer's account, triggered by a sector-wide review of networking equipment classification. The authority identifies the discrepancy.

- The authority issues a retroactive duty assessment for the difference between what was paid and what should have been paid across all affected shipments within the audit window.

- A penalty is calculated on top of the duty difference. Depending on the jurisdiction, this can represent a significant multiple of the original duty shortfall. The Importer of Record is issued formal notice of the full liability.

- The customs broker who filed the original declarations is not named in the assessment. The broker acted on the information they were given. The IOR, in whose name the entries were made, carries the full exposure.

In practice, such reassessments rarely apply to a single shipment. Customs authorities typically review all entries within the audit window where the same classification was used, multiplying the financial exposure across every affected shipment in that period.

The same pattern applies to valuation disputes, where declared transaction value does not match customs authority benchmarks, and to regulatory compliance gaps, where a required approval was not obtained before the shipment moved. In all cases, the liability follows the IOR.

The Paper IOR Problem

A paper IOR is an entity that allows its name to be used on import declarations without taking genuine operational responsibility for the compliance of those shipments. The entity exists on paper as the Importer of Record, but the actual compliance decisions, classification choices, and document management are handled elsewhere, typically by the shipper or a logistics provider operating informally in the IOR role.

This structure appears in markets where foreign companies cannot act as IOR directly and need a locally registered entity on the customs entry. In some cases the arrangement is deliberate. In others it emerges informally, where a local agent or distributor is listed as importer without any formal agreement about liability allocation.

The risk is direct. If a post-clearance audit identifies compliance failures in shipments carried under the paper IOR's name, that entity is the one receiving the assessment. Whether it has the financial capacity to absorb a substantial penalty, or the operational records to defend the classification decisions, depends on the specific arrangement. In many cases, neither is true.

From the foreign company's perspective, using a paper IOR arrangement does not eliminate exposure. It creates a layer of structural ambiguity that may or may not provide practical protection depending on the jurisdiction and the enforcement action. It does not eliminate the underlying compliance risk that created the liability. From a legal perspective, the paper IOR carries the liability. From a practical perspective, that risk may still cascade back to the foreign company through contractual disputes, financial claims, or operational disruption when the paper IOR cannot absorb the assessment. For a detailed explanation of this structure, see our guide on what a paper IOR is and why it creates risk.

What Proper IOR Structuring Actually Requires

For companies importing regulated goods into markets with meaningful compliance requirements, proper IOR structuring is an operational discipline, not a documentation formality.

It starts before the shipment moves. Classification has to be confirmed against the destination country's tariff schedule, not assumed from origin-country codes or supplier documentation. Regulatory approval requirements have to be identified and, where necessary, secured in advance. Document alignment between the commercial invoice, packing list, and customs entry has to be verified before the declaration is filed.

It continues after clearance. The Importer of Record should retain complete documentation for each import: the basis for classification decisions, the regulatory approvals obtained, and proof of duty and tax payment. This is the defense in a post-clearance audit. Without it, contesting an assessment is difficult regardless of whether the original declaration was correct.

And it requires choosing an IOR with genuine operational capacity in the relevant market. A locally registered entity with no customs infrastructure, no technical knowledge of the product categories it is importing, and no capacity to engage with regulatory authorities when issues arise does not provide meaningful compliance coverage. It provides a name on a form.

TFTIOR operates as a direct legal Importer of Record in the markets it covers. Pre-shipment classification review, regulatory approval coordination through BTK, TAREKS, TITCK, MCMC, and equivalent authorities in other markets, and post-clearance documentation traceability are standard operational functions. We assess every shipment before accepting it. If a jurisdiction, commodity classification, or document chain cannot be supported compliantly, we decline rather than create false comfort. That approach is why our accepted-shipment success rate is 100%.

Frequently Asked Questions

Who is responsible for import duties?

The Importer of Record is the entity legally responsible for payment of import duties. This applies regardless of commercial payment arrangements such as DDP Incoterms, and regardless of whether a freight forwarder or customs broker is involved in the shipment.

Does a customs broker assume import liability?

No. A customs broker acts as an agent that prepares and files customs declarations. Brokers do not assume legal liability for the accuracy of the import, the payment of duties, or regulatory compliance. Liability rests with the Importer of Record in whose name the declaration was made.

What happens if the HS code is wrong?

Incorrect HS classification can trigger retroactive duty reassessment, unmet regulatory compliance obligations, and financial penalties. Under Turkish Customs Law No. 4458, the penalty for a misclassification resulting in a duty shortfall is typically three times the difference between what was paid and what should have been paid. Post-clearance audits can surface classification errors months or years after clearance. The Importer of Record bears responsibility in all cases.

Does DDP shipping remove liability from the buyer?

No. DDP is a commercial Incoterm that defines who bears the cost of customs between buyer and seller. It does not change which entity carries legal liability under customs law. The entity named as Importer of Record on the customs entry remains the legally responsible party.

Can customs authorities audit a shipment after it has cleared?

Yes. Post-clearance audit powers exist in most jurisdictions and allow customs authorities to review import declarations after goods have entered the country. If issues are identified, the Importer of Record is subject to retroactive penalties and duty assessments regardless of when the original shipment cleared.

What is a paper IOR and why does it create risk?

A paper IOR is an entity that lends its name to import declarations without taking genuine operational responsibility for compliance. If customs authorities find errors in shipments carried under that name, the paper IOR carries the formal legal exposure. The foreign company's practical protection depends on the paper IOR's capacity to absorb the liability, which is often limited.

Structure Your IOR Correctly Before the Shipment Moves

If your shipment involves regulated equipment, cross-border deployment, or a non-resident import structure, defining the Importer of Record correctly is a compliance prerequisite, not an administrative step. TFTIOR operates as a direct Importer of Record with verified IOR coverage across 40 to 60 jurisdictions. Pre-shipment classification review, regulatory approval coordination, and post-clearance documentation traceability. MERSIS No. 0859123223400001. SSHYB No. 84634.

Related Resources

Importer of Record in Turkey: Complete Guide for Regulated Technology & Non-Resident Imports

A complete, execution-level guide explaining how Importer of Record works in Turkey for servers, telecom equipment, medical devices, and refurbished IT. Covers TAREKS workflows, BTK registration, customs timelines, pricing logic, and real operational risks for non-resident companies.

TFTIOR (Transparent DIS TICARET LTD.STI.) is a globally operating Importer of Record with verified IOR coverage across 40 to 60 jurisdictions. MERSIS No. 0859123223400001. SSHYB No. 84634 (Ministry of Trade After-Sales Service Authorization). TS 12498 qualified. ISO 9001, 14001, 45001 certified under IAS, an IAF MLA signatory accreditation body. UK operations line: +44 330 533 0223. Updated 2026.